How to handle your medical bills after a car accident in New York can feel overwhelming, especially when hospital costs exceed $61,000 for serious injuries. Emergency care, surgeries, and hospital stays create immediate financial pressure, while rehabilitation, therapy, and medications add to long-term expenses.

New York’s no-fault insurance law mandates PIP coverage for medical expenses, but it only pays up to policy limits. When costs go beyond coverage, the party responsible for paying medical bills in a car accident settlement depends on liability and legal action.

Dealing with insurance companies alone leads to delayed payments, low offers or denied claims. Victims without legal representation recover lower settlements, leaving them with unpaid bills. Legal options for covering medical expenses include third-party claims and lawsuits. Car accident lawyers help recover medical costs in NY by securing maximum compensation, eliminating financial stress, and ensuring victims receive full medical care without unpaid debt.

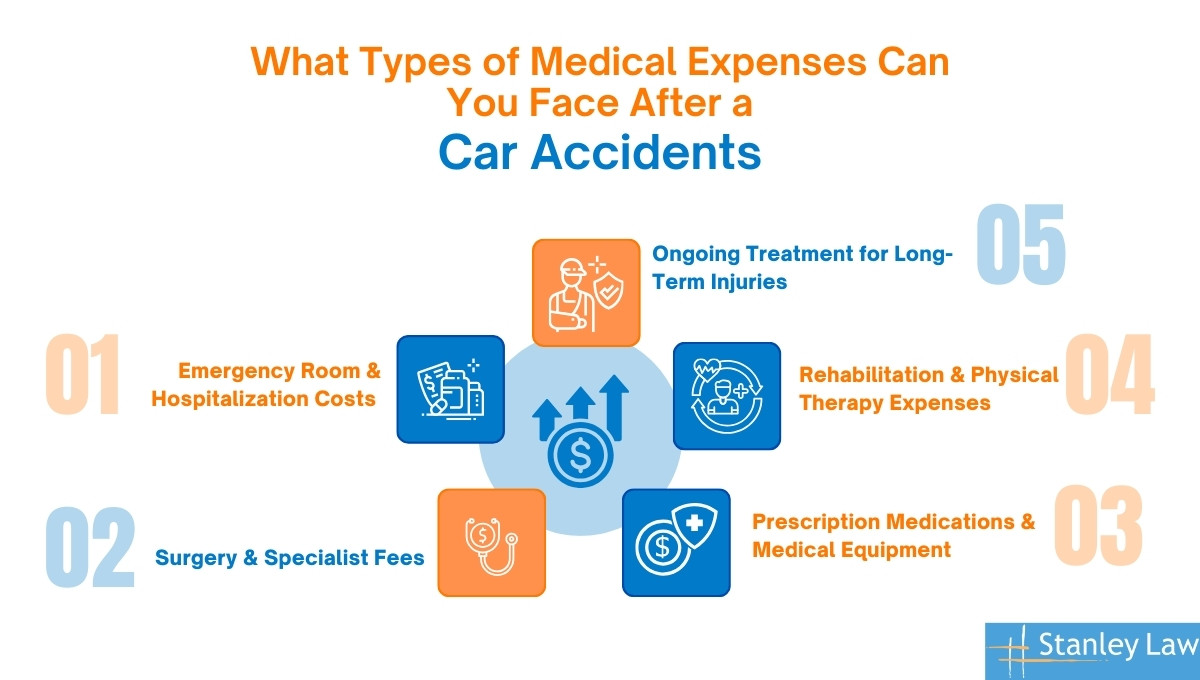

What Types of Medical Expenses Can You Face After a Car Accident?

The medical expenses you can face after a car accident depend on the severity of the injuries and the treatments needed. Below are the key types of expenses accident victims often deal with.

1. Emergency Medical Care and Hospital Stays

Emergency medical care after a car accident includes ambulance transport, ER treatment, diagnostic tests, and hospital admission. Costs vary based on hospital type, injury severity, and required treatments. ICU stays, trauma care, and specialized procedures significantly increase expenses.

- Hospital Type: Trauma centers charge more than general hospitals due to specialized staff and equipment.

- Injury Severity: Critical injuries require extended stays, advanced imaging, and intensive monitoring.

- Insurance Coverage: Policy limits determine out-of-pocket expenses, with higher deductibles increasing patient costs.

Immediate medical care is essential, but knowing the cost factors helps victims plan for financial recovery.

2. Surgery & Specialist Fees

Severe car accident injuries often require surgical procedures and specialist care, including orthopedic surgeries for fractures, neurosurgery for head or spinal injuries, and trauma procedures for internal damage. The complexity of these treatments significantly impacts costs.

- Procedure Type: More invasive surgeries, like spinal fusion or organ repair, require longer hospital stays and multiple specialists, increasing expenses.

- Medical Facility: Private hospitals and specialized trauma centers charge higher fees than public healthcare facilities.

- Post-Surgical Care: Follow-up visits, pain management, and physical therapy add to the total cost.

Surgical expenses are higher in metropolitan areas, where access to top specialists and advanced surgical equipment increases overall pricing.

Understanding these costs can help accident victims explore legal options for covering medical expenses.

3. Prescription Medications & Medical Equipment

Accident victims often need pain medications, antibiotics, and anti-inflammatory drugs during recovery. More severe cases may require assistive medical equipment such as wheelchairs, braces or prosthetics to regain mobility.

- Medication Type: Brand-name prescriptions cost significantly more than generic alternatives.

- Medical Equipment Customization: Standard devices are cheaper, while custom prosthetics and mobility aids increase costs.

- Insurance Coverage: Some policies restrict drug coverage or only cover basic medical equipment.

Medication and medical supply costs vary by region, with states like California and New York seeing higher prices due to pharmacy regulations and demand.

Knowing what medications and equipment are necessary helps victims manage expenses more effectively.

4. Rehabilitation & Physical Therapy Expenses

Recovery after an accident often requires physical therapy, occupational therapy, or chiropractic care to restore strength and mobility. Therapy sessions play a key role in preventing long-term complications.

- Injury Severity: More serious injuries require extended rehabilitation, sometimes months or years.

- Specialist Expertise: Licensed physical therapists with experience in post-accident recovery charge higher fees.

- Insurance Limits: Many health plans cap the number of covered therapy sessions, leaving patients with out-of-pocket expenses.

Rehabilitation services are more expensive in major cities, where the demand for specialized therapists increases costs.

Early therapy improves recovery and helps reduce long-term medical expenses.

5. Ongoing Treatment for Long-Term Injuries

Chronic pain, spinal injuries, and brain trauma often require long-term medical care, including pain management, specialist visits, and mental health therapy. Some victims need continuous treatment for years or even a lifetime.

- Injury Type: Conditions like spinal cord damage or traumatic brain injuries require lifelong treatment.

- Pain Management Approach: Ongoing treatments may include injections, physical therapy or surgery.

- Home Care Needs: Severe injuries may require professional caregivers or specialized living arrangements.

Long-term care is most expensive in metropolitan areas, where access to specialized medical providers increases demand and pricing.

Planning for long-term medical costs ensures accident victims receive the care they need without financial hardship.

Who Pays for Medical Bills in a Car Accident?

Personal Injury Protection (PIP) in New York covers initial medical expenses, regardless of fault. If medical costs exceed PIP limits, the at-fault driver’s insurance, third-party liability or health insurance pays the remaining costs.

If no insurance covers the full costs, accident victims pay out-of-pocket expenses, including deductibles, copays, and non-covered treatments. Legal claims against responsible parties provide compensation when other payment sources are exhausted.

When Does Auto Insurance Coverage Pay for Medical Bills?

New York’s Personal Injury Protection (PIP) pays medical expenses regardless of fault. This includes emergency care, hospital stays, surgeries, rehabilitation, and prescription medications. PIP applies to insured drivers and passengers and covers up to $50,000 per person per person.

PIP covers only medical costs and lost wages but does not include pain and suffering. If medical bills exceed PIP limits, accident victims use health insurance, at-fault driver liability or legal claims to pay the remaining expenses. If people do not have PIP coverage, they pay out-of-pocket costs unless another insurance policy applies.

When Does the At-Fault Driver’s Insurance Pay for Medical Bills?

The at-fault driver’s liability insurance covers medical bills when the injured party qualifies for a third-party claim under New York’s serious injury threshold. This applies to severe injuries, including fractures, disfigurement or permanent disability.

Liability insurance only pays for extended medical treatment, rehabilitation, and pain management if the victim proves the at-fault driver’s negligence. This coverage applies after PIP benefits are exhausted. If injuries do not meet the serious injury threshold, the victim cannot file a claim against the at-fault driver and must rely on PIP or health insurance for medical costs.

When Does Third-Party Liability Pay for Medical Bills?

Third-party liability applies when a business, government agency or vehicle manufacturer is responsible for the accident. This includes cases involving defective vehicle parts, hazardous road conditions or employer negligence.

When a third party is at fault, it covers hospitalization, surgeries, rehabilitation, and long-term medical care. The victim must prove negligence through a legal claim to secure compensation.

If no third party is found responsible, accident victims use PIP, health insurance or personal funds to cover medical expenses.

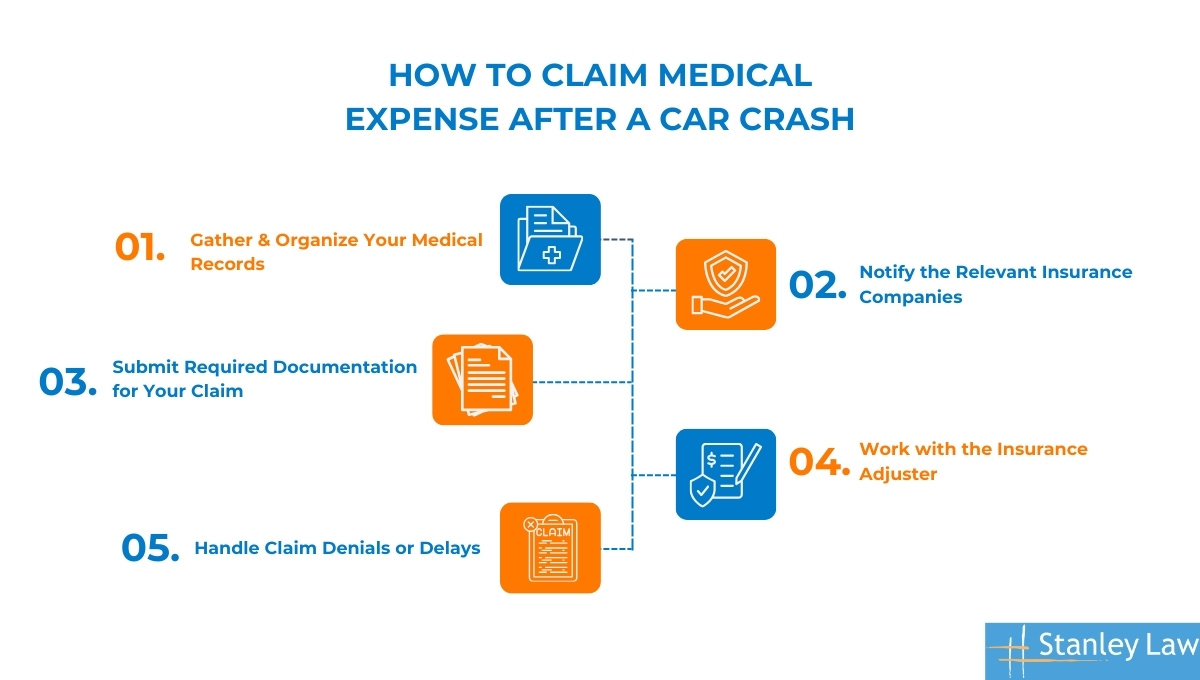

How to Claim Medical Expenses After a Car Crash?

Claiming medical expenses after a car accident requires following a structured process to maximize compensation. New York’s Personal Injury Protection (PIP) covers initial medical expenses, but if costs exceed limits, victims must seek additional compensation through at-fault driver liability, third-party claims or health insurance. According to the Insurance Research Council, victims who hire a lawyer recover 3.5 times more compensation, making legal representation a valuable asset in maximizing settlements.

Step 1. Gather & Organize Your Medical Records

- Request all medical records, including hospital bills, diagnostic reports, treatment plans, prescriptions, and rehabilitation summaries from healthcare providers.

- Ensure records are complete and accurate to avoid disputes over injury severity.

- Organize documents chronologically to establish a clear treatment timeline.

- Obtain proof of payment for all out-of-pocket expenses related to treatment.

- Expect the process to take 1 to 4 weeks, as some medical facilities delay record release.

Step 2. Notify the Relevant Insurance Companies

- Report the accident to your PIP provider, health insurer or the at-fault driver’s insurer within 24 hours to meet claim deadlines. It is important to report the accident to the proper authority as soon as possible.

- Provide only factual and necessary details to prevent adjusters from misinterpreting statements.

- Request written confirmation that the claim has been received and is being processed.

- Failure to notify insurers on time may result in claim denials or reduced payouts.

Step 3. Submit Required Documentation for Your Claim

- Prepare and submit complete paperwork, including medical bills, treatment reports, accident reports and wage loss statements.

- Verify that all documents match claim details to prevent discrepancies that can delay processing.

- Follow insurer-specific submission guidelines to ensure compliance with policy requirements.

- Keep copies of all submitted documents for reference in case of disputes.

- Monitor claim status through follow-ups to prevent unnecessary delays.

Step 4. Work with the Insurance Adjuster

- Expect an insurance adjuster to investigate your claim, review medical records and determine settlement amounts.

- Present well-documented medical evidence to justify treatment costs and ongoing care needs.

- Be cautious of low settlement offers aimed at minimizing payouts.

- Negotiate strategically instead of accepting the first offer, as initial settlements often undervalue long-term medical costs.

- Consult an attorney if the insurer disputes the claim or significantly undervalues expenses. Contact us to get a free consultation.

Step 5. Handle Claim Denials or Delays

- Review denial letters carefully to understand the reason for rejection.

- Gather evidence such as updated medical reports or doctor statements to strengthen the appeal.

- File an appeal within the required timeframe if the claim is unfairly denied.

- Seek legal assistance for complex claim denials or prolonged delays.

- Ignoring a denial results in paying out-of-pocket for medical expenses that should have been covered.

How Can Medical Bills Affect Your Car Accident Settlement?

Medical bills directly influence the final settlement amount in car accident claims. Insurance companies evaluate total medical expenses, severity of your car accident injuries and long-term care needs to determine compensation. Underestimating medical costs results in low settlements, leaving victims responsible for unpaid bills.

Insurance adjusters often dispute or minimize medical costs to reduce payouts. Personal injury lawyers help counter low offers, negotiate with providers and secure higher settlements. According to the Insurance Research Council, victims with legal representation receive 3.5 times more compensation than those who negotiate alone.

How Unpaid Medical Bills Affect Your Compensation?

Unpaid medical bills create financial pressure and lower the final settlement amount. When outstanding bills accumulate, hospitals and providers file medical liens, requiring repayment from settlement funds before victims receive compensation.

Insurance companies use unpaid bills to push lower offers, arguing that the victim’s medical care was excessive or unnecessary. Many accident victims accept quick, lowball settlements to avoid financial strain, leaving them with out-of-pocket expenses for future treatments.

To manage unpaid bills effectively, victims should keep detailed records, negotiate medical liens and work with the top car accident attorneys at Stanley Law Offices to ensure full reimbursement.

How Does Calculation from Insurance Adjusters Affect Your Compensation?

Insurance adjusters use internal formulas and software to calculate settlement amounts, often undervaluing claims. Their assessments consider medical bills, injury severity and projected recovery time, but they frequently challenge treatment costs to reduce payouts.

Adjusters may exclude certain treatments, downplay long-term care needs, or dispute medical necessity, resulting in lower compensation. Victims who rely solely on adjuster calculations risk settling for far less than their actual expenses.

To counteract these tactics, claimants should obtain independent medical evaluations, document all treatments and consult a New York car accident lawyer who can challenge the insurer’s calculations.

How Can Stanley Law Offices Help You in Recovering Medical Bills for Car Accidents Settlement?

- Maximizes Compensation – Lawyers calculate total damages, including medical expenses, lost wages and pain and suffering.

- Includes Long-Term Medical Costs – Attorneys factor in future treatments that insurance adjusters may ignore.

- Challenges Lowball Settlements – Insurers offer early low settlements, expecting victims to accept prematurely.

- Negotiates Medical Bills – Lawyers work with healthcare providers to lower outstanding medical liens.

- No Upfront Legal Fees – Personal injury lawyers operate on a contingency basis—clients pay only if they win.

Hiring a skilled New York personal injury lawyer increases your settlement and ensures you receive the full compensation you deserve, don’t let insurance companies undervalue your claim.